Tax saving mutual funds: when we mention them, usually what people would mention is equity-linked savings schemes, or ELSS. These schemes let you invest money in stock markets, with a tax break up to Rs 1.5 lakh under section 80C. And this investment is for three years only – PPF funds money for 15 years; even a tax-saving fixed deposit would invest the money for five years.

This blog covers what ELSS actually involves and how someone can start investing in it.

What Exactly Are Tax Saving Mutual Funds?

At their core, these are equity mutual funds that also qualify for a tax deduction, which is what separates them from a regular equity fund.

A fund manager takes money from a large pool of investors and puts most of it into stocks and equity-related instruments. Since these are market-linked, there’s no fixed return promised anywhere, unlike a fixed deposit where the number is locked in from day one.

A few things that define Tax Saving Mutual Funds:

- At least 65% of the portfolio has to sit in equities

- Three years is the lock-in, the shortest across all 80C instruments

- Returns move with the market; nothing is guaranteed

- Can be started as a lump sum or through monthly SIPs

Set this against PPF’s fifteen-year commitment or a tax-saving FD’s five years, and ELSS starts looking a lot more attractive for anyone who wants liquidity sooner rather than later.

How Do Tax Saving Mutual Funds Actually Work?

Once money goes into ELSS, it stays locked for three years while the fund manager actively trades stocks based on where the opportunities are.

There’s no early exit here. Even if the market dips hard six months in, the money can’t be pulled out before the three-year mark. Oddly enough, this restriction tends to work in the investor’s favor, since it removes the temptation to panic-sell during a rough patch.

Once three years pass, the units are fully redeemable. At that point, an investor can either take the money out or just leave it invested if the fund’s been performing well.

What Tax Benefits Do Tax Saving Mutual Funds Offer?

The headline benefit is a deduction of up to Rs 1.5 lakh under Section 80C, which brings down taxable income for that financial year.

This only applies under the old tax regime, though. Anyone who’s switched to the new regime won’t be able to claim this deduction at all, since Section 80C simply doesn’t exist there.

| Aspect | Details |

| Maximum Deduction | Up to Rs 1.5 lakh under Section 80C |

| Applicable Regime | Old tax regime only |

| Lock-in Period | 3 years |

| Tax on Gains After Lock-in | 10% LTCG tax above Rs 1 lakh profit |

Once the three-year lock-in ends, gains get treated as long-term capital gains, and anything above Rs 1 lakh profit in a financial year gets taxed at 10%.

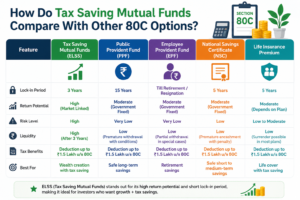

How Do Tax Saving Mutual Funds Compare With Other 80C Options?

The shorter lock-in is really what sets ELSS apart, along with the fact that it has real growth potential compared to fixed-return instruments.

| Investment | Lock-in Period | Average Returns | Risk Level |

| ELSS | 3 years | 12% to 15% | High |

| PPF | 15 years | 7% to 8% | Low |

| Tax-Saving FD | 5 years | 6% to 7% | Low |

| NSC | 5 years | 7% to 7.5% | Low |

Anyone who can handle some volatility usually comes out ahead with ELSS over a long enough timeframe. That said, someone who just wants their capital protected might still lean toward PPF or an FD, and there’s nothing wrong with that choice either.

How Can Someone Start Investing in Tax Saving Mutual Funds?

It starts with picking a fund, getting KYC done, and deciding whether to go with a lump sum or a SIP.

The process doesn’t differ much from investing in any other mutual fund, except there’s one extra thing to check – whether the fund actually qualifies for the tax benefit before putting money in.

Here’s roughly how it goes:

- Complete KYC using PAN, Aadhaar, and bank details

- Look at how the fund has performed over five to ten years, not just one

- Pick lump sum or SIP, whichever fits better

- Invest through an AMC website, an app, or a registered distributor

- Save the investment proof for filing returns later

A SIP tends to work better for people who don’t want to scramble for a lump sum every March. Spreading it across the year makes the whole thing a lot less stressful.

Are Tax Saving Mutual Funds Suitable for Beginners?

Yes, but only if the investor understands upfront that returns aren’t guaranteed the way they are with PPF or an FD.

Starting small through a SIP rather than jumping in with a lump sum makes the whole experience easier to manage. Monthly investments smooth out the highs and lows of the market automatically, so there’s less pressure to time anything perfectly. New investors should also resist picking a fund just because it had one strong year – that’s rarely the full picture.

A few things worth checking before investing:

- How the fund has performed across multiple market cycles, not just a recent good run

- The expense ratio, since higher fees quietly eat into returns

- Whether the fund manager has stayed consistent over time

- Whether a three-year lock-in actually fits your financial plans

Pages like r9wealth.com/mutual-fund/tax-saving-mutual-funds carry updated fund comparisons that can help narrow things down before investing.

This blog is meant for general understanding only and isn’t financial advice. Talking to a registered financial advisor before investing still makes sense, since everyone’s tax situation looks a little different.

Frequently Asked Questions

What is the lock-in period for Tax Saving Mutual Funds?

ELSS funds carry a mandatory three-year lock-in, the shortest among all Section 80C options.

Are Tax Saving Mutual Funds safe for conservative investors?

Not really, since these are equity-linked and carry market risk, unlike PPF or fixed deposits.

How much tax deduction can be claimed through ELSS?

Investors can claim up to Rs 1.5 lakh under Section 80C, but only under the old tax regime.

Can ELSS be redeemed before three years?

No, the three-year lock-in is mandatory and cannot be broken early under any circumstances.

Is SIP a good option for investing in Tax Saving Mutual Funds?

Yes, SIP spreads the investment across the year instead of requiring a large lump sum at once.

Follow us on Instagram, LinkedIn, Facebook and X (Twitter) for the latest mutual fund insights, SIP tips, investment strategies, and personal finance updates.